Download the Policybazaar app

to manage all your insurance needs.

Canara HSBC Saral Jeevan Bima is a comprehensive term insurance plan that covers people for a specific period. In the event of the insured person's unfortunate death during the policy term, the plan provides a lump sum death benefit to their nominees. This plan is specifically designed to cover individuals of all backgrounds, irrespective of educational qualification and occupation. Let’s understand the Canara HSBC Saral Jeevan Bima plan better in this article.

+Please note that the quotes shown will be from our partners

Here are the reasons why you should opt for the Canara HSBC Saral Jeevan Bima Plan:

The plan offers flexibility in choosing the Basic Sum Assured, Premium Payment Term, Policy Term, and Premium Payment Frequency according to the individual's insurance requirements.

Your loved ones get to enjoy Lump Sum Benefit on your unfortunate death.

The plan offers easy and hassle-free Purchase Process

Tax benefits under section 80C of the Income Tax Act, 1961 are available for this plan.

Here is the eligibility criteria for buying the Canara HSBC Saral Jeevan Bima Plan:

| Criteria | Minimum | Maximum |

| Entry Age | 18 years | 65 years |

| Maturity Age | 23 years | 70 years |

| Premium Payment Term | Under Single and Limited Payment: 5 to 10 years Under Regular Payment: Equal to Policy Term |

|

| Policy Term | Under Regular & Single Premium: 5 to 40 years Under Limited Premium (5 Pay): 6 to 40 years Under Limited Premium (10 Pay): 11 to 40 years |

|

| Sum Assured | Rs. 5 Lakhs | Rs. 25 Lakhs |

| Premium Payment Mode | Monthly, Half-yearly or Yearly | |

Listed below are the key features of the Canara HSBC Saral Jeevan Bima Plan:

Financial Security For Your Loved Ones: Ensure that your family is financially protected in case of any unfortunate event by choosing this insurance plan. It offers a lump sum benefit to your loved ones, helping them during difficult times.

Flexibility in Premium Payment Terms: You have the freedom to choose from various premium payment options. Whether you prefer a Single Premium, Limited Premium Payment for 5 or 10 years, or continuous premium payments throughout the Policy Term, the choice is yours.

Death Benefit: In the event of the Life Assured's death, a lump sum amount will be paid as the Death Benefit to the nominees/beneficiaries.

Tax Benefits: You can avail tax benefits under section 80C of the Income Tax Act, 1961.

Maturity Benefit: There are no maturity benefits provided under this plan.

Survival Benefit: There are no survival benefits offered by this plan.

**The Waiting Period is 45 days from the Date of Commencement of Risk. However, in the event of a policy revival, the Waiting Period will not be applicable.

Below mentioned are some of the policy details in the Canara HSBC Saral Jeevan Bima Plan:

Free Look Period: You have 15 days to review the policy after receiving it (30 days for electronic and distance marketing policies).

Grace Period: You get 30 days (for yearly and half-yearly) or 15 days (for monthly) to pay the premium after the due date.

Paid-Up Value: This plan does not have any paid-up value as it is solely for protection.

Surrender Value: There is no surrender value, but you may receive the policy cancellation value if you cancel it.

Revival Period: You can revive the policy within five consecutive years from the due date of the first unpaid premium.

Loan Facility: There is no loan facility available with this plan.

Lapsation of Policy: If the policy is not revived within the revival period, for regular premium, nothing will be payable, and for limited pay, you will receive the policy cancellation value.

Policy Cancellation Value:

Under Single Pay Policies: Policy Cancellation Value is available right after receiving the Single Premium and is calculated as follows:

70% of the Single Premium multiplied by (Unexpired Policy Term/Original Policy Term).

Under Limited Pay Policies: Policy Cancellation Value is available right after receiving the Single Premium, as follows:

70% * (Unexpired Policy Term/Original Policy Term).

Under Regular Pay Policies: The Policy Cancellation Value is not applicable in this plan.

Rebates For Females: The premium rates are determined based on a 3-year age setback.

Termination of Policy: The policy will terminate automatically under the following circumstances:

When the death benefit becomes payable.

When a refund, if applicable, is settled in case of policy cancellation.

On the maturity date of the policy.

If the policy is not revived by the end of the revival period.

Upon payment of the free look cancellation amount.

The following exclusion will be applied to the Canara HSBC Saral Jeevan Bima Plan:

Under Regular/Limited Pay Policies:

If the policyholder dies due to suicide within 12 months from the date of policy inception or revival, the following conditions apply:

If the policy is in-force at the time of death: The nominee will be entitled to receive 80% of the Total Premiums Paid until the date of death.

If the policy is revived before the suicide: The nominee will be entitled to receive 80% of the Total Premiums Paid until the date of death as available on the date of death.

After paying the above benefits, the policy will terminate. Please note that this provision applies specifically to death due to suicide within the first 12 months from the policy's inception or revival.

Under Single Pay Policies: If policyholder commits suicide within 12 months from the date of policy inception or revival, the following conditions apply:

The nominee will be entitled to receive 90% of the Single Premiums Paid (including any underwriting extra premium, if applicable) until the date of death.

Upon paying this benefit, the policy will terminate. Please note that this provision specifically applies to death due to suicide within the first 12 months from the policy's inception.

You may also like to read about term insurance

Note: Check all the best term insurance plan in India.

Note: You should also check the benefits of term life insurance if you are planning to purchase the term insurance plan.

˜The insurers/plans mentioned are arranged in order of highest to lowest Sum Assured(SA) offered by Policybazaar’s insurer partners offering term insurance plans on our platform, as per ‘first year premium of life insurers as at 31.03.2025 report’ published by IRDAI.

Policybazaar does not endorse, rate or recommend any particular insurer or insurance product offered by any insurer. For complete list of insurers in India refer to the IRDAI website www.irdai.gov.in

Rs. 400/month is starting price for a 1 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age, rounded off to nearest 10.

Rs. 400/month (Rs.13/day) is starting price for a 1 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 230 is starting price for a 50 lakhs term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age, rounded off to nearest 10.

+Rs. 8/day is starting price for a 50 lakhs term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age, rounded off to nearest 10.

+Rs. 12/day is starting price for a 75 lakhs term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age, rounded off to nearest 10.

+Rs. 497/month is starting price for a 1.5 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

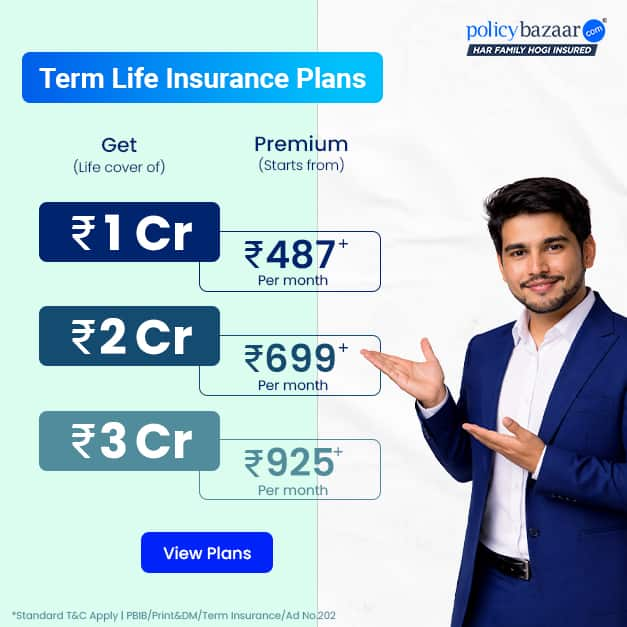

+Rs. 487/month is starting price for a 2 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 626/month is starting price for a 3 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 905/month is starting price for a 5 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. ₹361/month is the starting price for a ₹1 crore loan cover with an 8% interest rate for an 18-year-old male, non-smoker, with no pre-existing diseases, loan tenure up to 20 years, rounded off to the nearest 10

+Rs. 1,267/month is starting price for a 7 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

*The full refund of premium is available on availing the one-time option of refund of premium. Total premium paid for policy (paid for add-ons) will be the special exit value, payable on availing the one-time option of refund of premium if you wish to completely exit the policy.

+Rs. 447/month is starting price for a 1 crore term life insurance for an (NRI) 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs.679/month is starting price for a 2 crore term life insurance for an (NRI) 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 910/month is starting price for a 3 crore term life insurance for an (NRI) 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 1,374/month is starting price for a 5 crore term life insurance for an (NRI) 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 1,924month is starting price for a 7 crore term life insurance for an (NRI) 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

Women

+Rs. 400/month is Starting price for a 1 crore term life insurance for an 18 year-old Female, non-smoker, with no pre-existing diseases, cover upto 30 years of age, rounded off to nearest 10.

Rs. 461/month is the starting price for a 1 crore term life insurance for an 24 year-old female, non-smoker, with no pre-existing diseases, cover upto 54 years of age.

1,642/month is the starting price for a 1 crore term life insurance for an 44 year-old female, non-smoker, with no pre-existing diseases, cover upto 74 years of age.

Prices offered by the insurer are as per the approved insurance plans | #All savings and online discounts are provided by insurers as per IRDAI approved insurance plans | Standard Terms and Conditions Apply | **Tax Benefits are subject to changes in tax laws.| Policybazaar Insurance Brokers Private Limited

We will respond in the first instance within 30 minutes of the customers contacting us. 30-minute claim support service is for the purpose of giving reasonable assistance to the policyholder in pursuance of the claim. Settlement of claim (including cashless claim) is the responsibility of the insurer as per policy terms and conditions. The 30-minute claim support is subject to our operations not being impacted by a system failure or force majeure event or for reasons beyond our control. For further details, 24x7 Claims Support Helpline can be reached out at 1800-258-5881

For more details on risk factors, terms and conditions, please read the sales brochure carefully before concluding a sale

Policybazaar Insurance Brokers Private Limited | CIN: U74999HR2014PTC053454 | Registered Office - Plot No.119, Sector - 44, Gurgaon, Haryana – 122001 | Registration No. 742, Valid till 09/06/2027, License category- Composite Broker Visitors are hereby informed that their information submitted on the website may be shared with insurers. Product information is authentic and solely based on the information received from the insurers.

© Copyright 2008-2026 policybazaar.com. All Rights Reserved

˜ Policybazaar Promise reflects the guarantee offered by insurers. Price assurance is based on certifications shared by insurers with us.

Insurance

Calculators

Resources

Payment Methods

Secured With

Follow us on