Download the Policybazaar app

to manage all your insurance needs.

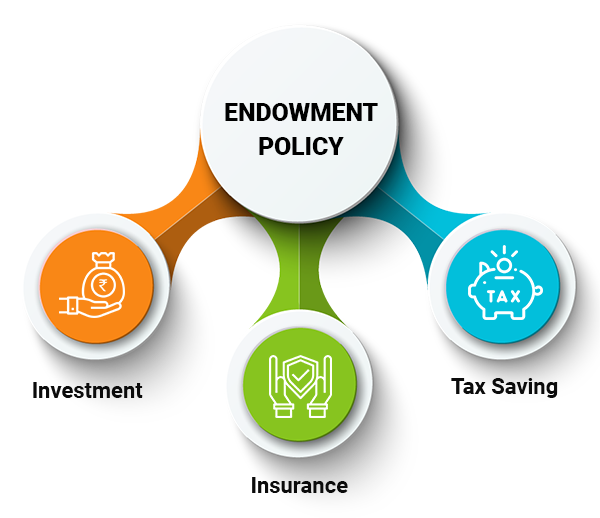

An endowment policy is a life insurance plan that combines both protection and savings. It offers financial security by providing a lump sum payment either upon the policy's maturity or in the event of the policyholder's death during the term. This dual benefit makes it a valuable tool for achieving long-term financial goals such as education, buying a home, or retirement planning while safeguarding loved ones

Save upto ₹46,800 in tax under Sec 80C^

Inbuilt Life Cover

Tax Free Returns^

Fully Tax-Free, Life Cover Included

Below are the steps on how this savings plan works:

| Endowment Policies | Entry Age (Min-Max) | Maturity Age (Min-Max) | Premium Paying Term (PPT) |

| Private Insurer | |||

| SBI Life - Shubh Nivesh | 18 years | 60 years | 10 to 30 years |

| HDFC Life Sanchay Plus | 18 years | 60 years | 5, 6, 10 and 12 years |

| Axis Max SWP-Long Term Income | 18 years | 60 years | 5,6,8,10 and 12 years |

| Axis Max SWAG-Long Term Wealth | 18 years | 60 years | 5, 6, 8, 10 and 12 years |

| ICICI Pru GIFT Pro- Increasing Income with ROP | 18 years | 60 years | 5, 6, 7, 8, 9, 10, 11 and 12 years |

| Bajaj Life Guaranteed Wealth Goal - Second Income with ROP | 18 years | 60 years | 5, 6, 7, 8, 10 and 12 years |

| Aditya Capital Assured Income Plus – Income with Lumpsum Benefit | 18 years | 60 years | 5, 6, 8, 10 and 12 years |

| Canara HSBC iSelect GFP-LTI with ROP | 18 years | 65 years | 5, 7 and 10 years |

| Star Union Dai-ichi Life Jeevan Ashray | 18 | 70 years | Equal to term or 10 years |

| India First Life Mahajeevan Plus | 5 | 70 years | 5/7/9/10/12/15 years |

| Shriram Life New Shri Life Plan | 30 days | 75 years | 5 - 25 years |

| Reliance Nippon Life Endowment Plan (Regular Premium) | 5 years | 75 years | Equal to policy term (10–25 yrs) |

| Ageas Federal Life Guaranteed Savings Plan | 2 years | 55 years | Single Pay (7/10 years policy) |

| Bharti Axa Life Super Endowment Plan | 8 years | 75 years | 8–15 years |

| Edelweiss Tokio Life Premier Guaranteed Income Plan | 18 years | 23–99 years (depends on variant) | 5, 8, 10, 12 years |

| Future Generali Life New Assured Wealth Plan | 18 years | 71 years | Limited Pay (option-dependent) |

| Pramerica Life Smart Income Plan | 8 years | 75 years | 5, 8, 10, 12 years |

| Bandhan Life Premier Endowment Insurance Plan | 18 years | 60 years | 8 years (for 10-year term PT) |

| Aviva Life Wealth Builder Endowment Plan | 5 years | 67 years | Single, 5/10 years |

| Go Digit Life Endowment Plan | 18 years (typically) | 85 years | Regular/Limited/Single Pay |

| CreditAccess Life Nitya Sanchay Micro Endowment | 18 years | 75 years | Policy Term = PPT |

| Public Insurer | |||

| LIC Jeevan Utsav | 18 years | 50 years | 5 to 16 years |

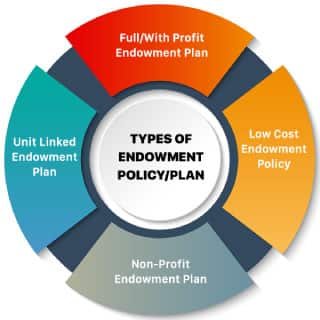

A Unit Linked Endowment Plan seamlessly blends life insurance with market-based investments. Your premiums are allocated between providing life cover and investing in a selection of market-linked funds. You can actively manage and switch between these funds to align with your investment goals. The potential returns depend on how your chosen funds perform, offering opportunities for growth but also carrying associated risks.

This traditional endowment policy invests your premiums and, over time, accumulates bonuses. These bonuses, declared by the insurer based on their profits, are added to your assured sum and become guaranteed once announced. This approach combines guaranteed insurance coverage with the potential for steadily growing returns.

Designed primarily to help repay a mortgage or loan, the Low-Cost Endowment offers life insurance cover while targeting enough savings to settle your outstanding debt by the end of the policy term. Its structure allows for lower premiums compared to standard endowment plans, making it an affordable solution for borrowers seeking both protection and savings.

A Non-Profit Endowment policy focuses on delivering a fixed, guaranteed payout at the end of the term or a death benefit, with no additional bonuses. This plan prioritizes certainty by providing a clear, predetermined maturity amount or benefit to your beneficiaries.

Guaranteed endowment policies assure a specific sum will be paid to you on maturity or to your beneficiaries in the event of your passing. Face value is provided regardless of market conditions. While this policy may include non-guaranteed bonuses, its primary advantage lies in the security of the guaranteed payout, combined with the possibility of extra returns if bonuses are declared.

This policy allows you to enjoy endowment benefits while paying premiums for only a limited period. Coverage remains active for the entire policy term, making it appealing for those who want comprehensive protection and savings without a long-term payment commitment.

Money-Back Endowment Policies provide periodic payouts throughout the policy duration, instead of a single lump sum at maturity. This structure adds liquidity to your insurance-savings plan, ensuring you receive regular cash benefits while still maintaining life cover for the entire term.

Endowment policies give you the following benefits:

A reversionary bonus is an annual addition to the sum assured of your policy. Once declared and added, it becomes a permanent part of your policy benefits and is payable at maturity or upon the death of the insured. This bonus cannot be withdrawn or reduced as long as the policy remains active until one of these events.

A terminal bonus is a one-time, lump sum reward paid at the end of the policy term—either upon maturity or on the occurrence of a claim (such as the policyholder’s death). It reflects the long-term investment performance of the insurer and is given as an extra benefit for remaining invested for the full policy term.

To enhance your endowment plan, you can choose from several rider options:

Salient features of the endowment policy are:

There are a few limitations associated with an Endowment insurance policy, which are mentioned below:

Sum Assured: Upon the maturity of an endowment policy, you are entitled to receive the sum assured, which is the guaranteed amount set during the policy purchase.

Bonuses: If you have chosen a profit-based plan, any bonuses or additional profits accumulated over the policy term are included in the final payout.

Tax-Free Benefits: The maturity amount received by you is generally exempt from taxes under Section 10(10D) of the Income Tax Act, provided certain conditions, such as premium limits, are satisfied.

People Seeking Dual Benefits: Suitable for those who want both life insurance and a savings component in a single plan.

Financially Disciplined Individuals: Endowment plans offer a disciplined route to build a corpus for dependents in case of financial contingencies

Long-Term Savers: Small businesspersons, salaried individuals, lawyers, and doctors should consider buying endowment plans for long-term financial goals

Tax-Saving Investors: Great for individuals looking to save on taxes, as the premiums paid and the maturity benefits are eligible for tax deductions.

Risk-Averse Individuals: Endowment plans are ideal for risk-averse individuals who do not mind settling for fewer returns and are not super-rich.

Endowment policies provide a disciplined means of saving money for future needs.

An additional advantage is life-risk coverage for the family and dependents of the policyholder.

Returns may be lesser, but they are risk-free for a certain sum assured.

Tax benefits can be availed under Sections 80C and 10(10D), subject to certain conditions.

Risk-averse investors prefer endowment plans.

It offers life insurance coverage to the insured in case of an unforeseen event.

It offers the maturity amount to the policyholder if she/he survives the policy term.

One should see the following things before purchasing an endowment plan:

Begin Early Planning: Making investments at an early age offers a long horizon to invest. It promotes disciplined saving and offers better returns through compounding.

Review the Flexibility Option: Choose based on your income. Regular pay options suit salaried individuals, while single-pay options work for those with irregular incomes.

Know Different Types of Endowment Policies: Know the different endowment plans. Part of the premium goes to life insurance, and the rest is invested based on whether the plan is profit-based or non-profit.

Select a Plan that Offers Riders: A lot of insurance companies offer additional benefits like accidental death benefit or critical illness.

Bonuses: Bonuses depend on the insurer’s profits and are distributed at the end of each policy year.

Non-Guaranteed and Guaranteed Returns: Endowment policies offer both guaranteed and non-guaranteed returns, giving you the benefit of savings and risk-free insurance.

The beneficiary should inform the insured about the death soon after the death of the policyholder. As soon as the insurer gets to know about the loss, a claim form is forwarded to the nominee.

To claim the death benefit, the beneficiary/nominee of the policyholder/assignee or legal heirs must sign the claim form.

The last treating doctor who checked the insured should provide the loss statement.

The hospital authorities where the insured received treatment should provide the certificate.

A witness statement and death certificate from someone present during cremation are required.

If the insurance company requires a discharge voucher, it should be filled out and provided.

For effective and fast sanction of the death benefit, an additional form, as mentioned below, should be provided:

Post Mortem’s certified copy, police investigation report, and First Information Report – in the situation of the death of the policyholder was unnatural.

Employer’s e-certificate, if the insured was working in an organization.

The key differences between an endowment policy and term plan are as follows:

| Feature | Term Plan | Endowment Plan |

| Purpose | Pure protection; offers life cover only | Combines life cover with savings |

| Premium | Lower premiums | Higher premiums |

| Maturity Benefit | No maturity benefit (unless a rider is added) | Provides a lump sum on policy maturity |

| Death Benefit | The death benefit is paid if the insured passes away during the policy term | Death benefit along with savings component paid to beneficiaries |

| Investment Component | No investment component | Offers savings and investment along with life cover |

| Suitable For | People looking for affordable life cover | People looking for life cover plus savings or investment |

| Policy Term | Typically shorter (5-30 years) | Can be long-term (10-30 years) |

| Tax Benefits | Available under Section 80C and 10(10D) | Available under Section 80C and 10(10D) |

The common differences between an endowment assurance policy and ULIP plans are:

| Parameter | Endowment Policy | ULIP Plans |

| Definition | A life insurance policy that combines insurance coverage and a savings component | A life insurance policy that provides insurance coverage along with market-linked investment options |

| Return on Investment | Fixed returns with guaranteed bonuses | Varies based on the market performance of the underlying investment |

| Maturity Benefit | Guaranteed sum assured along with accrued bonuses | Market-linked returns based on the fund's performance |

| Death Benefit | Sum assured + accrued bonuses | Higher of the sum assured or fund value |

| Tax Benefits | Deductions on premiums paid and tax-free maturity amount up to a certain limit. | Premiums up to Rs. 1.5 lakhs are eligible for tax deductions under Section 80C. The maturity amount is tax-free under Section 10(10D) if annual premiums paid are less than Rs. 2.5 lakhs. |

| Liquidity | Limited options for withdrawal before maturity | The flexibility of fund withdrawal after the lock-in period also allows fund switching. |

| Risk | Low-risk investment option | The risk profile depends on the chosen market-linked funds |

| Ideal for | Risk-averse investors looking for guaranteed returns | Investors willing to take on market risks and seeking higher returns |

Mentioned below is the list of documents required for an endowment assurance policy in different situations:

There are two types of tax benefits for endowment plans that policyholders, nominees, and potential buyers should know.

Premium Deduction: You can claim a deduction on the premiums paid in your endowment assurance policy under Section 80C of the Income Tax Act 1961. The deduction is limited to a maximum of Rs 1.5 lakhs per year.

Benefits Exemption: Under Section 10(10D) of the Income Tax Act 1961, tax exemption can be claimed on the benefits received from the endowment plan. This includes both the maturity benefit and the death benefit. However, specific conditions must be satisfied to qualify for this exemption.

The following table presents an overview of the best endowment assurance policy types for different situations:

| Situation | Best Endowment Policy Type |

| Guaranteed Payouts with Low Risk | Guaranteed Endowment Policy |

| Higher Returns with Market Exposure | Unit-Linked Endowment Policy |

| Long-Term Savings with Life Cover | With Profit Endowment Policy |

| Flexible Premiums and Coverage | Limited Premium Pay Endowment Policy |

| High Liquidity Needs | Money Back Endowment Policy |

| Tax Benefits | Unit-Linked Endowment Policy |

27 Jul 2026

In India, most households keep gold in lockers, without earning

30 Jul 2026

The SBI Gold Monetisation Scheme is a practical solution for

27 Jul 2026

Physical gold is a headache to store and comes with purity risks

˜The insurers/plans mentioned are arranged in order of highest to lowest first year premium (sum of individual single premium and individual non-single premium) offered by Policybazaar’s insurer partners offering life insurance investment plans on our platform, as per ‘first year premium of life insurers as at 31.03.2025 report’ published by IRDAI. Policybazaar does not endorse, rate or recommend any particular insurer or insurance product offered by any insurer. For complete list of insurers in India refer to the IRDAI website www.irdai.gov.in

Disclaimer:##The Guaranteed Returns are dependent on the policy term and premium term availed along with other variable factors. 7.4% rate of return is for an 18-year-old, healthy male for a policy term of 20 years and a premium term of 10 years with ₹5,00,000 annually installment premium. All plans listed here are from insurance companies’ funds. The tax benefits under Section 80C allow a deduction of up to ₹1.5 lakhs from the taxable income per year and 10(10D) tax benefits are for investments made up to ₹2.5 Lakhs/ year for policies bought after 1 Feb 2021. Tax benefits and savings are subject to changes in tax laws.

*All savings are provided by the insurer as per the IRDAI approved

insurance plan.

+ Trad plans with a premium above 5 lakhs would be taxed as per

applicable tax slabs post 31st march 2023

#Discount offered by insurance company. Standard T&C Apply

^Section 80C allows annual deductions of up to ₹1.5 lacs from the taxable income. Section 10(10D) provides tax-free maturity benefits for investments of up to ₹2.5 Lacs/ year, on policies bought after 1 Feb 2021. Tax benefits and savings are subject to changes in tax laws.

++Source - Google Review Rating available on:- http://bit.ly/3J20bXZ

Insurance

Calculators

Payment Methods

Secured With

Follow us on