Download the Policybazaar app

to manage all your insurance needs.

SUD Life Saral Jeevan Bima is an individual, non-participating and non-linked, life insurance plan. It offers financial protection for the insured person and his family in the event of unfortunate circumstances as a pure risk premium plan. This plan is a standard, term life insurance plan for individual coverage, with simple features and easy to understand terms and conditions.

A recent spike has been seen in the preference of the customer when it comes to the pure term life insurance plans due to their affordability and convenience. So, in order to meet the growing demands of the customers, innovative protection products have been introduced by life insurance companies with different benefits, options, terms, and so forth. The Insurance Regulatory and Development Authority of India (IRDAI) has introduced standardized term insurance product to help the customers make an informed choice.

SUD Life Saral Jeevan Bima is a very transparent and easy to apprehend policy that will pay the particular nominee a fixed sum of money after the death of the policyholder. The plan does not discriminate against the issuance of the policy on the basis of gender, occupation, place of residence, educational qualification, and not even in the case of restriction in travel.

Let’s take a look at the eligibility criteria of the policy.

|

Eligibility Criteria |

Details |

||

|

Maximum |

|

Minimum |

|

|

Entry Age |

18 years |

|

65 years |

|

Maximum Maturity Age |

70 years |

||

|

Life cover |

Rs. 5,00,000 |

|

Rs. 25,00,000 |

|

Single premium |

4,070 |

|

66,200 |

|

Annualized premium |

1,130 |

|

88,875 |

|

Policy terms |

5 years |

|

40 years |

|

Premium payment term (years) |

Single, regular pay, 5 pay, & 10 pay |

||

|

Premium payment terms modes |

Single, yearly, half-yearly, and monthly |

||

|

Loan facility |

A loan facility is not provided under this policy. |

||

SUD Life insurance company provides a plethora of benefits that make its policies popular and attract many policy bearers in the country. The categories in which SUD life provides benefit are given as follows:

In case of the demise of the policyholder, given it has happened within the policy term, Sum Assured on Death will immediately be paid to the insured’s beneficiary or the nominee. Amount insured on demise will be paid in lump sum figures. The sum assured to the policyholder is subjected to the premium payment terms (years) of the policy.

All conditions are as follows:

1. In the case of Regular pay, 5 pay and 10 pay

Sum Assured on death will be the highest of these amounts:

Annualized Premium refers to premium paid in a year excluding rider premiums, underwriting additional premiums, taxes, and modal premium loadings.

Total Premiums Paid means all the premiums paid by the policyholder and received by the Company, excluding any rider premium, extra premium, and taxes.

2. In the case of Single Premium

Sum Assured on Death is higher of the:

125% of the Single Premium OR the Absolute Amount Assured on death, where the following condition will be observed:

Tax benefits:

Tax benefits will be available as per the applicable tax laws of the Indian Income Tax Act. Good and Service Tax (GST) of 18% will also be applicable.

Optional Rider Benefit

SUD Life SaralJeevanBima policy has the provision in which an approved accident benefit and the permanent disability rider can be attached.

The riders are add-on coverage offered by the policy to enhance the coverage of the policy. It can be added to the applied policy by paying some extra sum along with the premium sum of the policy. The Rider Sum Assured will be paid in case of any occurrence covered under the rider takes place, as per the rider's prescribed conditions.

The process to purchase SUD life SaralJeevanBima is very easy. After administering quick research from the eligibility table, the customer can decide to purchase the policy. One can buy the policy in both online and offline mode easily. Steps one needs to take to purchase are given below:

Online Process

Offline Process

The documents required to buy the SaralJeevanBima policy are only an indicative requirement. The policyholder may be asked for additional documents if the policy issuers find anything which can serve as an obstacle in the issuance of the policy. Only copies of the officially valid documents which are attested by the policyholder are accepted. The following documents are required to purchase this SUD life policy:

Exclusions mentioned under the SUD life SaralJeevanbima only include under the case of suicide cases. In the case of suicide of the policyholder, the conditions are different in a single premium policy and a regular or a limited premium policy. All terms are given as follows:

1. Single premium policy

This policy shall be considered null and void if the life assured dies by suicide at any time within a year from the date of risk commencement of the policy. The Insurer will not entertain any claim, and the death benefit will be 90% of the single premium paid. This will exclude any extra amount charged by the Insurer on account of taxes, underwriting, and rider premium.

2. Regular/limited premium policy

This policy shall be considered null and void if the life assured dies by suicide at any time within a year from the risk commencement date, provided the policy is active or within a year from the policy revival date. The Company will only pay a sum that equals 80% of the premium paid as a death benefit to the nominee.

You may also like to read about term insurance

Note: Check all the best term insurance plan in India.

Nomination is the process of designating a person to receive the policy money payable under life insurance policy upon the happening of the risk event specified in the policy. The nominee is authorized only to give a valid discharge to the policy proceeds when the claim is payable.

If the premium is not paid within the days of grace, then the policy lapses. Typically, the days of grace for policies with the monthly mode of payment is 15 days, and for all other modes, it is one month, not less than 30 days.

Suppose there is an emergency and the policyholder does not wish to continue with the policy. In that case, one can cancel the policy anytime within the Policy tenure, provided the Policy has acquired the Cancellation Value. In case of Limited Premium Payment Policies, the policyholder has to cancel the policy before the end of its term, or the maturity date, or at the end of revival period if the policy is not revived,

The premium depends upon the policy holder’s gender, age, selected sum assured, premium payment term and mode, and policy term. The following modal factors are applied to the annualized premium:

Yearly = 1

Half-yearly = 0.5108

Monthly = 0.0867

˜The insurers/plans mentioned are arranged in order of highest to lowest Sum Assured(SA) offered by Policybazaar’s insurer partners offering term insurance plans on our platform, as per ‘first year premium of life insurers as at 31.03.2025 report’ published by IRDAI.

Policybazaar does not endorse, rate or recommend any particular insurer or insurance product offered by any insurer. For complete list of insurers in India refer to the IRDAI website www.irdai.gov.in

Rs. 400/month is starting price for a 1 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age, rounded off to nearest 10.

Rs. 400/month (Rs.13/day) is starting price for a 1 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 230 is starting price for a 50 lakhs term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age, rounded off to nearest 10.

+Rs. 8/day is starting price for a 50 lakhs term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age, rounded off to nearest 10.

+Rs. 12/day is starting price for a 75 lakhs term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age, rounded off to nearest 10.

+Rs. 497/month is starting price for a 1.5 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

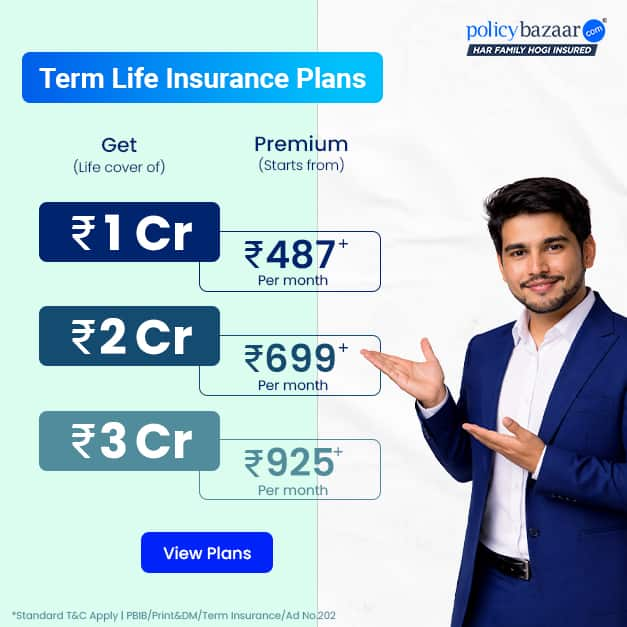

+Rs. 487/month is starting price for a 2 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 626/month is starting price for a 3 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 905/month is starting price for a 5 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. ₹361/month is the starting price for a ₹1 crore loan cover with an 8% interest rate for an 18-year-old male, non-smoker, with no pre-existing diseases, loan tenure up to 20 years, rounded off to the nearest 10

+Rs. 1,267/month is starting price for a 7 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

*The full refund of premium is available on availing the one-time option of refund of premium. Total premium paid for policy (paid for add-ons) will be the special exit value, payable on availing the one-time option of refund of premium if you wish to completely exit the policy.

+Rs. 447/month is starting price for a 1 crore term life insurance for an (NRI) 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs.679/month is starting price for a 2 crore term life insurance for an (NRI) 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 910/month is starting price for a 3 crore term life insurance for an (NRI) 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 1,374/month is starting price for a 5 crore term life insurance for an (NRI) 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 1,924month is starting price for a 7 crore term life insurance for an (NRI) 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

Women

+Rs. 400/month is Starting price for a 1 crore term life insurance for an 18 year-old Female, non-smoker, with no pre-existing diseases, cover upto 30 years of age, rounded off to nearest 10.

Rs. 461/month is the starting price for a 1 crore term life insurance for an 24 year-old female, non-smoker, with no pre-existing diseases, cover upto 54 years of age.

1,642/month is the starting price for a 1 crore term life insurance for an 44 year-old female, non-smoker, with no pre-existing diseases, cover upto 74 years of age.

Prices offered by the insurer are as per the approved insurance plans | #All savings and online discounts are provided by insurers as per IRDAI approved insurance plans | Standard Terms and Conditions Apply | **Tax Benefits are subject to changes in tax laws.| Policybazaar Insurance Brokers Private Limited

We will respond in the first instance within 30 minutes of the customers contacting us. 30-minute claim support service is for the purpose of giving reasonable assistance to the policyholder in pursuance of the claim. Settlement of claim (including cashless claim) is the responsibility of the insurer as per policy terms and conditions. The 30-minute claim support is subject to our operations not being impacted by a system failure or force majeure event or for reasons beyond our control. For further details, 24x7 Claims Support Helpline can be reached out at 1800-258-5881

For more details on risk factors, terms and conditions, please read the sales brochure carefully before concluding a sale

Policybazaar Insurance Brokers Private Limited | CIN: U74999HR2014PTC053454 | Registered Office - Plot No.119, Sector - 44, Gurgaon, Haryana – 122001 | Registration No. 742, Valid till 09/06/2027, License category- Composite Broker Visitors are hereby informed that their information submitted on the website may be shared with insurers. Product information is authentic and solely based on the information received from the insurers.

© Copyright 2008-2026 policybazaar.com. All Rights Reserved

˜ Policybazaar Promise reflects the guarantee offered by insurers. Price assurance is based on certifications shared by insurers with us.

“I have opted for Term insurance plan of PNB MetLife. This is

Read more

ICICI Pru Saral Jeevan Bima is a simple term insurance plan that

Read more

The LIC Saral Jeevan Bima Premium Calculator is a tool that

Read more

The Future Generali Saral Jeevan Bima offers a safety net

Read more

The SBI Life- Saral Jeevan Bima is a non-linked and

Read moreInsurance

Calculators

Payment Methods

Secured With

Follow us on