Are Fibre Parts of Your Bike Covered Under Your Bike Insurance Policy?

- Home

- Motor Insurance

- Bike Insurance

- Articles - TWI

- Are Fiber Parts of Your Bike Covered Under Your Bike Insurance Policy?

When purchasing or renewing a two-wheeler insurance policy, many riders assume that every damaged component of their bike will be fully covered. However, the reality is slightly more nuanced. Understanding what parts are covered under bike insurance is essential because claim payouts depend on the type of material,depreciation rules, and whether you have opted for bike insurance add-on covers. Bike parts insurance is governed by standard depreciation norms followed by insurers in India under the regulatory framework of the regulatory. These norms determine how much of the repair cost the insurer will actually pay at the time of settlement.Lets understand this in detail.

What Parts Are Covered Under Bike Insurance?

Under a comprehensive two-wheeler insurance policy, coverage extends to the bikes own damage caused by accidents, fire, natural calamities, vandalism, or theft. This includes major structural and mechanical components such as the engine assembly, gearbox, chassis, fuel tank, suspension system, and electrical wiring. Damage to headlights, indicators, digital consoles, and other factory-fitted electrical parts is also generally covered if the loss occurs due to an insured event.

Body panels, which include metal, fibre, and plastic components, are also covered under comprehensive coverage. However, while these parts are insured, the claim amount payable depends heavily on depreciation. This is where many policyholders get confused.

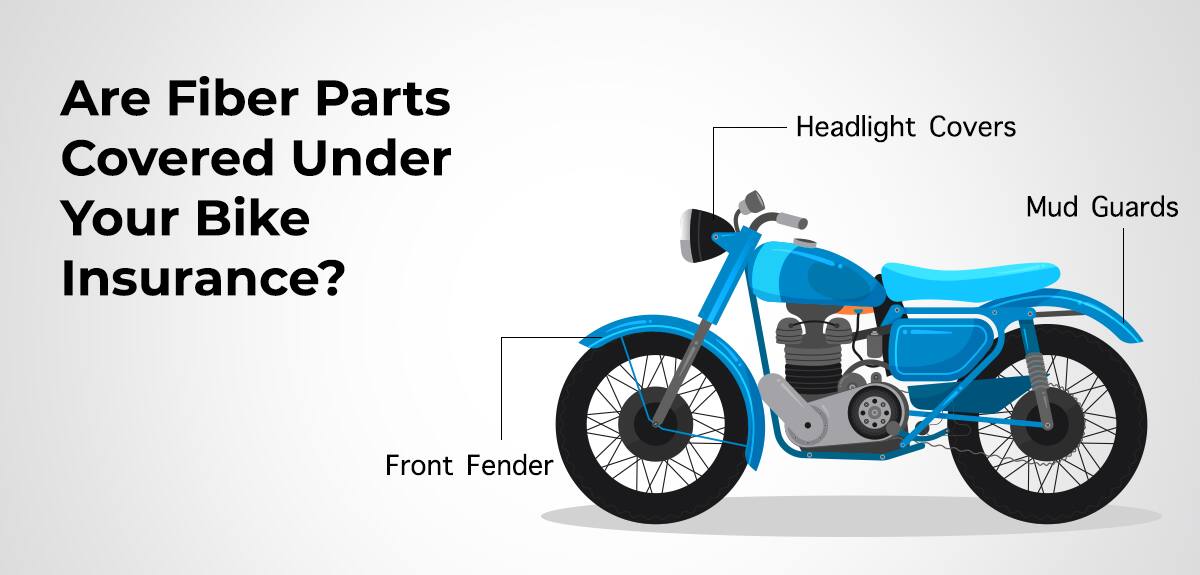

Are Fibre Parts Covered Under Bike Insurance?

Yes, fibre parts are covered under bike insurance, but the claim payout depends on the type of policy you have and whether depreciation applies.

Under a comprehensive two-wheeler insurance policy, damage to fibre components such as front and rear cowls, side panels, mudguards, and other fibre-glass body parts is covered if the damage is caused by an insured event like an accident, fire, natural calamity, or vandalism.

However, while fibre parts are included in bike parts insurance, they are not reimbursed at full value under a standard policy. As per depreciation norms followed by insurers, fibre-glass parts generally attract around 30% depreciation at the time of claim settlement.

Lets understand this with the help of an example:

If a fibre body panel replacement costs ₹10,000, the insurer may deduct 30% (₹3,000) as depreciation. The remaining ₹7,000 is payable by the insurer, subject to policy deductible. The balance amount has to be paid by the policyholder.

So, even though fibre parts are covered under bike insurance, the reimbursement is partial unless you have opted for zero depreciation cover.

Are Bike Alloy Wheels Covered in Bike Insurance?

Another commonly searched query is whether bike alloy wheels are covered in insurance. The answer depends on whether the alloy wheels are factory-fitted or aftermarket modifications.

If the alloy wheels were fitted by the manufacturer at the time of purchase, they are typically covered under the own-damage bike insurance policy or a comprehensive bike insurance policy. If they are damaged in an accident, you can claim insurance for bike repair involving alloy wheels, subject to policy terms and depreciation.

However, if the alloy wheels were installed later as an aftermarket modification and not declared to the insurer, the claim may be rejected. To ensure coverage for modified parts, they must be declared and endorsed in the policy by paying an additional premium.

Can We Claim Bike Insurance for Bike Repair?

Yes, you can claim bike insurance for bike repair if the damage is caused by an insured event such as an accident, fire, flood, cyclone, or theft. However, routine wear and tear, mechanical breakdown without external impact, and consumable items are generally not covered.

It is also important to follow the correct procedure when filing a claim. Many claims are delayed or partially settled because proper steps were not followed.

How to Raise Bike Insurance Claim?

If your bike is damaged, the first step in understanding how to claim two-wheeler insurance is to inform your insurer immediately. Most insurers allow claims to be registered online or through customer care. Once the claim is registered, the insurer appoints a surveyor to inspect and assess the damage.

It is important not to start repairs before the surveyors inspection unless it is an emergency. You will be required to submit documents such as your RC copy, driving licence, policy document, and photographs of the damage. In cases involving theft or third-party injury, an FIR may also be required.

After inspection and approval, repairs can be carried out at a network garage if you want a cashless claim. The insurer will then settle the approved amount directly with the garage, and you will need to pay the depreciation amount and deductibles. This is the standard process for how to claim insurance for bike repairs in India.

How Depreciation Impacts Bike Parts Insurance?

Depreciation is the most significant factor that affects your final claim payout. Even though parts are covered under bike insurance, the insurer reduces the payable amount based on the material type and age of the vehicle.

For instance, if your total repair bill is ₹20,000 and plastic parts worth ₹8,000 are replaced, 50% depreciation may apply to those parts. After adding compulsory deductible, your out-of-pocket expense can become substantial. This is why understanding depreciation in advance helps in setting realistic expectations during claims.

What is Zero Depreciation Cover?

Zero depreciation (also known as Nil Dep) is an add-on cover that eliminates depreciation deductions on eligible parts. With this add-on, plastic and fibre parts are reimbursed without applying the standard depreciation percentage. As a result, the claim payout is significantly higher.

This add-on is particularly useful for new bikes, premium motorcycles, and riders who frequently travel in heavy traffic areas where minor accidents are more common. Although the premium increases slightly, the reduction in out-of-pocket expenses during claims often makes it worthwhile.

What is Not Covered Under Bike Parts Insurance?

Even the comprehensive bike policy has exclusions. Damage due to regular wear and tear, electrical or mechanical breakdown without accidental cause, riding under the influence of alcohol, and undeclared modifications are typically excluded. Engine damage due to water ingression may also not be covered unless you have opted for an engine protection add-on.

Understanding these exclusions is as important as knowing what parts are covered under bike insurance.

FAQs – Are Fiber Parts of Your Bike Covered Under Your Bike Insurance Policy?

-

Q. What is not covered in bike insurance?

Ans. Bike insurance does not cover wear and tear, mechanical breakdown, riding without licence, intoxication, racing, or undeclared modifications. Consumables are also excluded. -

Q. Does bike insurance cover accessories?

Ans. Factory-fitted accessories are covered. Aftermarket accessories are covered only if declared and endorsed in the policy. -

Q. Can I claim insurance for bike dents?

Ans. Yes, if you have comprehensive coverage. Minor dents may not be worth claiming due to deductible and depreciation. -

Q. Are tyres, battery, and broken parts covered?

Ans. Yes, but tyres usually have 50% depreciation. Battery and broken parts are covered if damaged due to an insured event. -

Q. Can I use my bike after 15 years?

Ans. Yes, only if you renew registration and obtain a valid fitness certificate from the RTO.

Note: Few pointers you need to keep remember always