Download the Policybazaar app

to manage all your insurance needs.

In many Indian homes, a housewife is the one who keeps everything running smoothly. From managing the household and looking after children to planning daily expenses, her role supports the entire family. While this work does not come with a salary, replacing it would involve real costs. It makes sure that if something unexpected happens, the family has financial support to manage childcare, household help, and daily responsibilities without disruption. It is a practical way to protect the life your family depends on every day.

Term insurance for housewife is a type of life insurance plan which provides for payments to the family of the housewife in the event of the housewife's unfortunate death. The payment terms in the plan are guaranteed to the nominee/claimant in return for the premium payments paid on time by the policyholder. The plan provides a very high coverage value for a low premium, ensuring the financial requirements of the family members are satisfied without any hassle of managing money. Various payment schemes can be opted for, which include a lump sum payment, monthly payments, among others in a joint payment plan. The housewife term insurance plan will keep the house running as usual, in the absence of the housewife.

The following are the best term insurance plans for housewives available in India in {{CURRENTYEAR}}. You can compare the term insurance plan for housewife based on their premiums, sum assured, benefits offered, or the requirement of your husband’s income proof to find the right term insurance plan without income proof for yourself.

| Private Insurer | Term Insurance Plan for Housewife | Husband’s Income Proof | Sum Assured | |

| HDFC Life Insurance | HDFC Life Click 2 Protect Super | Not Required | 50 Lacs - 20 Crores | |

| ICICI Prudential Life Insurance | ICICI Pru iProtect Smart | NA | 50 Lacs – 20 Crores | |

| Tata AIA Life Insurance | Tata AIA Sampoorna Raksha Promise | Not Required | 25 Lacs – No limit | |

| SBI Life Insurance | SBI Life eShield Next | NA | 50 Lacs – No limit | |

| Bajaj Life Insurance | Bajaj Life eTouch II | Not Required | 50 Lacs – No limit | |

| Axis Max Life Insurance | Axis Max Smart Term Plan Plus | Not Required | 25 Lacs – 20 Crores | |

| Go Digit Life Insurance | Digit Glow Term Insurance | NA | 25 Lacs – 1 Crore | |

| Aditya Birla Sun Life Insurance | ABSLI DigiShield | NA | 30 Lacs – No limit | |

| India First Life Insurance | India first Life Plan | NA | 1 Lac - 50 Crores | |

| Kotak Mahindra Life Insurance | Kotak e-Term Insurance | NA | 51 Lacs - No limit | |

| Canara HSBC Life Insurance | Canara HSBC Young Term Plan - Life Secure | NA | 25 Lacs – No limit | |

| Shriram Life Insurance | Shriram Life Online Term Plan | NA | 25 Lacs - 10 Crores | |

| PNB Met Life Insurance | PNB Mera Term Plan Plus | Required | 25 Lacs - No limit | |

| Star Union Dai-ichi Life Insurance | SUD Life e-Lifeline | NA | 25 Lacs - 1 Crore | |

| Pramerica Life Insurance | Pramerica Life Saral Jeevan Bima | NA | 5 Lacs - 25 Lacs | |

| Aviva Life Insurance | Signature 3D Term Plan - Platinum | NA | 30 Lacs - 5 Crores | |

| Future Generali Life Insurance | Future Generali Care Plus Plan | NA | 10 Lacs - No limit | |

| Reliance Nippon Life Insurance | Reliance Nippon Life Super Suraksha Plus | NA | 2 Crore - No limit | |

| Ageas Federal Life Insurance | Termsurance Life Protection Insurance Plan | NA | 5 Lacs - No limit | |

| Bandhan Life Insurance | Bandhan Life iTerm Prime | NA | - | |

| Bharti Axa Life Insurance | Bharti AXA Flexi Term Pro | NA | 25 Lacs - No limit | |

| Edelweiss Life Insurance | Edelweiss Life Zindagi Protect Plus | NA | 50 Lacs – No limit | |

| Public Insurer | ||||

| Life Insurance Corporation of India | LIC Jeevan Amar | NA | 25 Lacs - No Limit | |

*The insurers/plans mentioned are arranged in order of highest to lowest Sum Assured(SA) offered by Policybazaar’s insurer partners offering term insurance plans on our platform, as per ‘first year premium of life insurers as at 31.03.2025 report’ published by IRDAI. Policybazaar does not endorse, rate or recommend any particular insurer or insurance product offered by any insurer. For complete list of insurers in India refer to the IRDAI website www.irdai.gov.in

* The above table represents the plans available for a 25 year old, non-smoker housewife looking for a 50 lakh life cover, with the husband’s annual income between 10-15 Lakhs, covering her till 60 years of age.

Term insurance plan is definitely the need of the hour for housewives. Considering the increasing prevalence of diseases among women, such as PCOD (polycystic ovarian syndrome) and breast cancer, housewives may need term insurance to ensure their families are financially secure in case of an unforeseen death.

The best term insurance plan for housewife can help the beneficiaries/nominee through the guaranteed coverage amount that can aid in expenses like existing loans, education, etc.

It supports your financial planning by offering the beneficiary/nominee a guaranteed amount to deal with important expenses.

It is ideal in terms of providing a corpus for family members.

Not only that, but several life insurance companies offer special benefits for female customers, like Max Life introduced its Term plan for Housewife and Bajaj Allianz provides health management services up to 36.5K via health checkups, including cancer screenings, diabetic, thyroid, and lipid profile tests, OPD consultations, nutrition, diet, and psychologist consultations, and medicine network discounts.

You can choose the best term insurance for housewife in the following ways:

Choose the Adequate Cover: Since the life cover is the amount that will be paid to your family in your absence, you should choose a cover large enough to cover their needs financially. It is highly recommended that you should check your financial plans.

Compare Premiums: When selecting a term insurance for housewife, always compare premium rates from multiple insurers. This helps make sure you get maximum cover at a premium that fits within your family’s budget without compromising on policy features.

Add Available Riders: Many plans offer important term insurance riders like critical illness, accidental death benefit, or waiver of premium. These riders enhance the basic term insurance for housewife by offering extra protection in specific situations. You should add riders that match your health profile and family history.

Choose a Policy with Long-Term Benefits: Since a housewife often handles long-term responsibilities like childcare and elder care, opt for a term insurance for housewife with a long policy term, this provides continued protection while your dependents are still financially reliant on you.

Return of Premium (ROP) Plan: you’re looking for value at maturity, choose a Return of Premium variant. This type of term insurance for housewife refunds the total premiums paid if the policyholder survives the policy term. This plan is usually selected by families who want some return at the end of the policy.

Check Claim Settlement Ratio: The Claim Settlement Ratio (CSR) is an important consideration when buying a term insurance plan. The CSR is calculated easily by dividing the total number of death claims received by the insurance company by the number of death claims that were settled.

Select the Right Type of Plan: Select the right type of term insurance plan, as this will make sure your family receives the benefit amount and the insurer returns the premiums back at the maturity of the policy.

Here are some of the benefits of term insurance for housewives:

Fixed Sum Assured: A housewife's contribution to the family is priceless, even if it can't be measured in money. People often forget about the cost of hiring help to do household chores, but it can put a strain on the family budget. This unplanned cost could put a strain on your finances. A term plan for a housewife gives her family a steady income while she's gone, which helps them handle their money well and reach their future goals without any extra stress.

Financial Safety for family: A housewife may not have a large financial contribution to the family, but her contributions in different areas are invaluable. Purchasing term insurance for housewife guarantees financial stability by offering a death benefit that could save your loved ones. This payment can help the family in managing financial constraints and covering important future expenses.

Affordable premiums: The premiums for term insurance for housewives are highly affordable, starting from just ₹481 for a 1 Crore term insurance cover. You can always use the term insurance calculator in order to calculate your insurance premium amount for your chosen term plan.

Life Stage Cover Enhancements: With a term insurance for housewives, you can increase coverage as your family grows. As new members join the family, financial needs also rise, especially for goals like children's education and marriage. To keep up with these changes, it's important to adjust the sum assured so that your coverage is enough for the family’s growing needs. This option makes sure that your plan adapts to inflation and the family’s changing financial demands.

Cover for Spouse: The spouse is usually the primary earner in the family. If the spouse passes away unexpectedly, it can cause financial stress. A term plan for housewife can make sure that the non-earning member is also financially secure in case of the husband's untimely death.

Critical Illness Coverage: Serious illnesses like heart disease, cancer, or kidney failure can lead to large medical expenses. By adding a critical illness rider to the term plan, you get a lump-sum payout if diagnosed with a covered illness. For housewives, the plan can offer coverage for women-specific illnesses, such as cervical or breast cancer, providing added protection.

Flexibility: Term insurance for housewife helps housewives customize products to fit their budget. For instance, you can easily choose to pay the premiums in a way that works for you, such as single, limited, or regular pay term with monthly, annual, semi-annual, or quarterly premium pay mode. You can also choose to get your money all at once, every month, every month plus a lump sum, or every month plus a growing amount.

Tax Benefits: You can get tax benefits for term insurance under sections 80C and 10(10D) of the Income Tax Act, 1961. Always talk to your financial advisor to find out what tax breaks you can get with your term insurance.

Tax Benefits: You can claim term insurance tax benefits as per the prevailing tax laws under sections 80C and 10(10D) of the Income Tax Act, 1961. You should always consult with your financial advisor to see the tax benefits you can avail with your term insurance.

Peace of Mind: Term insurance for housewife allows the family to lead a stress-free life. The children can use the payout to pay for their long-term goals, like pursuing higher education or getting married.

Benefits for Children: The financial benefit from the term insurance plan for housewife can be helpful in planning for the future of their child, including their marriage, higher education, and other expenses. This will guarantee a stress free life from financial constraints for her children.

Term insurance for housewife offers several advantages that help secure your family's financial future. Here's how it can support your loved ones:

Financial Protection

The main advantage of term insurance is the financial security it may bring to your family in case something unfortunate happens to the policyholder. It allows your family to pay for household expenses, medical bills, and other financial emergencies that may arise.

Income Replacement

Term insurance can replace the income of the main earner by offering the payout as monthly installments. This helps the family manage living costs and maintain financial stability in the absence of the primary income source.

Debt Repayment

A term insurance payout can help your family if you have any debts that are still unpaid. It can be used to pay off loans or mortgages, which can help you avoid financial stress when times are tough.

Achieving Financial Goals

Term insurance can also help fulfill long-term financial goals, such as funding your child's education or their future wedding. It makes sure that the family's dreams are not compromised, even in your absence.

Spouse’s Retirement

A term life insurance payout can help the dependent spouse become financially independent in the long run. It gives them money to make sure they can live comfortably in retirement, even if the main breadwinner is no longer around.

Secure Your Family Future Today

₹1 CRORE

Term Plan Starting @

Get an online discount of upto 15%#

Compare 40+ plans from 15 Insurers

Here are some of the features of the term plan for housewife:

You can purchase a high sum assured amount at very low premium rates. This is mainly because a term plan for housewife is a pure protection policy with no component of investment. The entire premium amount is used to provide the life cover that is paid to the nominee upon demise during the policy tenure.

The term insurance for housewife has increased additional term cover benefits. This feature gives policyholders the option to increase the policy coverage during the policy term, considering the husband has also opted for a term plan. The housewife term insurance offers benefits for the well-being of their children, allowing them to guarantee their child’s bright future without any financial stress. For example, if a husband has a term cover of 1 crore and then the wife buys a term plan for housewife for a life cover of 50 Lakhs. Then, the total sum of 1.5 crores will help in securing your children’s future.

Another benefit that most of the life insurers provide is waiver of premium. This feature waives off the premium payment if the policyholder becomes critically ill, injured, or physically impaired. These are the situations in which the policyholder will not be required to pay the premium amount.

A term plan also offers the return of premium option, wherein the premium amount paid will be returned by the insurer subject to the plan terms and conditions as a maturity payout to the policyholder.

The term plan for housewife can easily be bought for a longer policy term, ensuring family’s financial protection at any time.

An individual can now easily access various term plans, assess their features and choose the best term insurance for housewife. In addition to this, buying a term plan, paying a premium amount, submitting a claim, and other processes are quite easy and cost-effective.

Choosing the right life cover (sum assured) in your term plan is important for your family's financial protection. This amount provides important protection in case of unforeseen circumstances, providing you peace of mind. A high amount makes sure your family are supported very well, covering debts/loans, income replacement, and education costs. Choosing the right amount is important to make sure their family’s future is secure. To check the best term life insurance plans, you can find the right sum assured for your financial needs by clicking on the below options.

Term Plans

Terminal Illness: Terminal illness payout, or accelerated death payout, is offered by insurance companies when the life assured is diagnosed with a condition likely to lead to death within 6 months from the date of diagnosis during the policy term. However, if the diagnosis occurs within the last 12-18 months of the policy, early payout may be excluded since death could happen after the policy ends. In such cases, death benefits are still provided to the family, but an early payout isn't an option.

Waiver of Premium: Another benefit offered by numerous life insurance companies in India is the waiver of premium riders. This feature, as the name suggests, waives all the remaining premiums in case of a critical illness or permanent disability. In other words, there are circumstances where the policyholder is not obligated to make premium payments. This becomes relevant when an accident or disability prevents the policyholder from meeting premium obligations.

Critical Illness Rider: If the policyholder is diagnosed with a critical illness, such as heart stroke, cancer, the critical illness rider offers an additional or accelerated payout that helps the policyholder pay for the treatment costs or medical expenses. This is an optional benefit that can be added to the base plan at nominal premiums.

Accidental Death Benefit: A housewife can add extra riders to her term life insurance policy to protect against death caused by accidents. The policyholder can add the accidental death benefit rider to the base term plan to get more coverage. If the policyholder dies in an accident, the term insurance rider will pay out more money.

When you compare term insurance for a housewife, you can find the plan that fits your family's needs and stays within your budget. Different plans have different benefits, like how much coverage they offer, how much the premiums are, and how you can get your money, like in a lump sum or on a regular basis. You can find the best plan with the most value by comparing them. Some plans even come with extra benefits like critical illness riders or premium waivers. This guarantees that your family's financial protection is complete and meets your needs.

The term insurance plan for a housewife is necessary to bring financial security to the family in the event of her untimely death. A housewife’s contribution to the family may not be financial, but it is irreplaceable. The term insurance plan also recognizes the contribution made by a housewife. Here are the reasons why term insurance plan for a housewife is important:

Financial Security for the Family

In the absence of a housewife, handling household expenses, children, etc., becomes a challenging task. Term insurance for housewives is very essential in ensuring that the family is in a position to cope with the challenges.

Covers Non Monetary Contributions

Housewives play an important role in managing the home, raising children, and supporting the family. While these contributions cannot be financially measured, term insurance compensates for their value, making sure that the family can afford professional help if needed.

Affordable Premiums for High Cover

Housewives can benefit by obtaining large sum assured at low premium costs, with easier planning of adding term insurance to the budget, ensuring that the women enjoy long-term cover without putting a burden on the budget of the family.

Here is a step-by-step guide on how to buy a term plan for housewife from Policybazaar:

Step 1: Visit Policybazaar and go to their term insurance for housewife page.

Step 2: Fill in all the required details like name, contact number, and date of birth. Then, click on ‘View Plans’.

Step 3: Answer the basic questions about occupation type, annual income, educational qualification, and smoking habits.

Step 4: After submitting all this information, a list of all available term insurance plans for housewife will be displayed

Step 5: Select the term insurance plan for housewife and then proceed to pay.

Nowadays, women are facing a number of health concerns like breast cancer, PCOD, and sometimes an unforeseen demise during childbirth. This is the time that women should think about long-term financial planning, which is why term insurance for housewife is need of the hour.

A term insurance plan offers various benefits, such as adding riders, tax savings, affordable premiums, critical illness coverage, and guaranteed financial support for appointed beneficiaries to cover essential expenses. A term insurance comparison can help you select the ideal plan by checking premiums and features.

Here are some of the things you should look into before buying a housewife term insurance:

Make sure the life cover chosen is adequate: Always check if the sum assured amount is sufficient to secure your family members in case of an unfortunate incident. As per the general thumb rule, you can consider the cover amount to be 3-5 times the annual salary of the husband.

Consider your expenses: Consider the child's education plans, loans, liabilities, and family expenses before deciding the life cover for term insurance for housewives.

Wife can use Husband’s Income Proof: A working wife can easily buy term insurance for women using her income proof and other documents requested by the insurer.

Current medical condition: The family can decide if adding a health rider is important by taking into account the health of a housewife and the medical history of her family.

Keep the Type of Term Plan in Mind: There are different types of term insurance plan for housewives that are offered when purchasing term insurance. You should choose the term plan that suits your requirements and financial objectives among these options due to their difference in features.

˜The insurers/plans mentioned are arranged in order of highest to lowest Sum Assured(SA) offered by Policybazaar’s insurer partners offering term insurance plans on our platform, as per ‘first year premium of life insurers as at 31.03.2025 report’ published by IRDAI.

Policybazaar does not endorse, rate or recommend any particular insurer or insurance product offered by any insurer. For complete list of insurers in India refer to the IRDAI website www.irdai.gov.in

Rs. 400/month is starting price for a 1 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age, rounded off to nearest 10.

Rs. 400/month (Rs.13/day) is starting price for a 1 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 230 is starting price for a 50 lakhs term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age, rounded off to nearest 10.

+Rs. 8/day is starting price for a 50 lakhs term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age, rounded off to nearest 10.

+Rs. 12/day is starting price for a 75 lakhs term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age, rounded off to nearest 10.

+Rs. 497/month is starting price for a 1.5 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 487/month is starting price for a 2 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 626/month is starting price for a 3 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 905/month is starting price for a 5 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. ₹361/month is the starting price for a ₹1 crore loan cover with an 8% interest rate for an 18-year-old male, non-smoker, with no pre-existing diseases, loan tenure up to 20 years, rounded off to the nearest 10

+Rs. 1,267/month is starting price for a 7 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

*The full refund of premium is available on availing the one-time option of refund of premium. Total premium paid for policy (paid for add-ons) will be the special exit value, payable on availing the one-time option of refund of premium if you wish to completely exit the policy.

+Rs. 447/month is starting price for a 1 crore term life insurance for an (NRI) 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs.679/month is starting price for a 2 crore term life insurance for an (NRI) 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 910/month is starting price for a 3 crore term life insurance for an (NRI) 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 1,374/month is starting price for a 5 crore term life insurance for an (NRI) 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 1,924month is starting price for a 7 crore term life insurance for an (NRI) 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

Women

+Rs. 400/month is Starting price for a 1 crore term life insurance for an 18 year-old Female, non-smoker, with no pre-existing diseases, cover upto 30 years of age, rounded off to nearest 10.

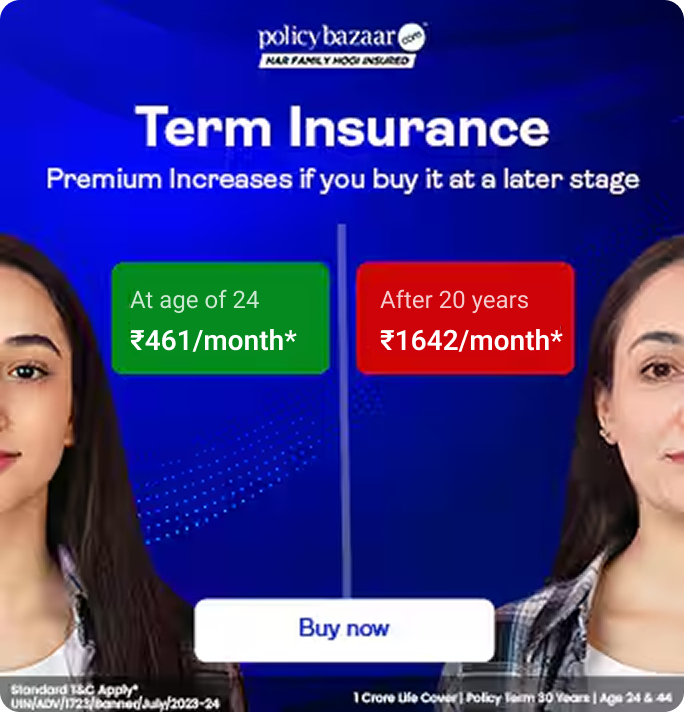

Rs. 461/month is the starting price for a 1 crore term life insurance for an 24 year-old female, non-smoker, with no pre-existing diseases, cover upto 54 years of age.

1,642/month is the starting price for a 1 crore term life insurance for an 44 year-old female, non-smoker, with no pre-existing diseases, cover upto 74 years of age.

Prices offered by the insurer are as per the approved insurance plans | #All savings and online discounts are provided by insurers as per IRDAI approved insurance plans | Standard Terms and Conditions Apply | **Tax Benefits are subject to changes in tax laws.| Policybazaar Insurance Brokers Private Limited

We will respond in the first instance within 30 minutes of the customers contacting us. 30-minute claim support service is for the purpose of giving reasonable assistance to the policyholder in pursuance of the claim. Settlement of claim (including cashless claim) is the responsibility of the insurer as per policy terms and conditions. The 30-minute claim support is subject to our operations not being impacted by a system failure or force majeure event or for reasons beyond our control. For further details, 24x7 Claims Support Helpline can be reached out at 1800-258-5881

For more details on risk factors, terms and conditions, please read the sales brochure carefully before concluding a sale

Policybazaar Insurance Brokers Private Limited | CIN: U74999HR2014PTC053454 | Registered Office - Plot No.119, Sector - 44, Gurgaon, Haryana – 122001 | Registration No. 742, Valid till 09/06/2027, License category- Composite Broker Visitors are hereby informed that their information submitted on the website may be shared with insurers. Product information is authentic and solely based on the information received from the insurers.

© Copyright 2008-2026 policybazaar.com. All Rights Reserved

˜ Policybazaar Promise reflects the guarantee offered by insurers. Price assurance is based on certifications shared by insurers with us.

If you are looking for a simple, affordable way to financially

Read more

Accidental Death and Dismemberment Insurance can be a great way

Read more

Heart attack vs cardiac arrest is a comparison many people

Read more

Most people think that a term insurance policy will pay out if

Read more

When responding to a heart attack, every passing second counts

Read moreInsurance

Calculators

Payment Methods

Secured With

Follow us on