Download the Policybazaar app

to manage all your insurance needs.

The Government of India has initiated various schemes to offer basic healthcare facilities to Indian citizens. The Pradhan Mantri Jeevan Jyoti Bima Yojana and Pradhan Mantri Suraksha Bima Yojana are two such schemes introduced by the government.

The schemes are specifically designed to provide healthcare facilities to low-income families in India. The schemes aim to provide immediate relief to the families in case of an unfortunate demise of the life assured.

Pradhan Mantri Suraksha Bima Yojana provides coverage for accidental death and disability, and Pradhan Mantri Jeevan Jyoti Bima Yojana provides coverage for death due to other reasons. In this article, we will discuss the similarities and differences between both schemes in detail.

PMSBY full form is Pradhan Mantri Suraksha Bima Yojana. The scheme is offered by Public Sector General Insurance Companies (PSGICs) and other general insurance companies. It is an Accident Insurance Scheme that provides one-year cover and is renewable from year to year.

The Pradhan Mantri Suraksha Bima Yojana Scheme provides insurance for accidents, including death, disability, and permanent disability. Anyone who is aged 18 to 70 and has a bank account can join this scheme. The yearly premium for Pradhan Mantri Suraksha Bima Yojana stands at Rs 12, and it will be automatically deducted from the linked bank account. If you are completely disabled or die in an accident, your nominee gets Rs. 2 Lakhs. If you have a partial permanent disability from an accident, you receive Rs. 1 Lakh.

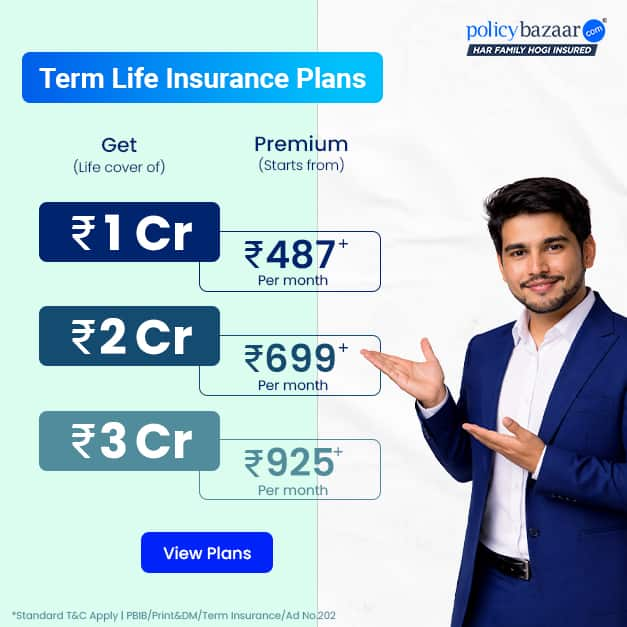

Term Plans

Pradhan Mantri Jeevan Jyoti Bima Yojana is a government scheme that was launched in 2015. This life insurance scheme offers financial help to the policyholder’s family members in case of his/her unfortunate death. This scheme is offered by LIC, other life insurers, and Indian banking institutes. It is available for individuals from 18 years to 50 years with savings bank accounts at official banks. The annual premium for the Pradhan Mantri Jeevan Jyoti Bima Yojana amounts to Rs 330, and it will automatically be deducted from your linked bank account. If the claimant has several savings accounts in different banks, then he/she can enroll under the PMJJBY Scheme through one savings account only. It is much like a term insurance plan that provides protection during unforeseen events.

*Note: The annual premiums of PMJJBY and PMSBY may fluctuate based on your location, the prevailing GST rates, and your age.

The following table elaborates the key differences between PMJJBY and PMSBY:

| Parameters | Pradhan Mantri Jeevan Jyoti Bima Yojana | Pradhan Mantri Suraksha Bima Yojana |

| Scheme Type | PMJJBY is a life insurance scheme | PMSBY is an accidental insurance scheme |

| Age Limit | The minimum age limit for Pradhan Mantri Jeevan Jyoti Bima Yojana is 18 years and maximum is 50 years. | The minimum age limit for the Pradhan Mantri Suraksha Bima Yojana is 18 years and maximum is 70 years. |

| Premium | The annual premium for the Pradhan Mantri Jeevan Jyoti Bima Yojana scheme is Rs. 330. The premium amount could differ depending on the age, location and prevailing income tax laws. | The annual premium for Pradhan Mantri Suraksha Bima Yojana is Rs. 12. Note that the premium amount could differ based on the age, location and prevailing income tax laws. |

| Coverage | According to Pradhan Mantri Jeevan Jyoti Bima Yojana, the death cover of the life assured will be provided irrespective of the cause of demise. The amount would be paid to the beneficiary/nominee in case of life assured’s death. | Pradhan Mantri Suraksha Bima Yojana offers coverage for disability or death due to accidents. The amount would be payable to the nominee/beneficiary in case of policyholder’s death. |

| Benefits | In the event of the unfortunate death of the life assured, the policy's beneficiary receives Rs. 2 Lakhs as death benefit. |

|

Secure Your Family Future Today

₹1 CRORE

Term Plan Starting @

Get an online discount of upto 15%#

Compare 40+ plans from 15 Insurers

Listed below are the similarities between PMJJBY and PMSBY:

Both these schemes are government backed insurance schemes and can be purchased by all Indian residents, regardless of their income. PMJJBY and PMSBY schemes were launched by the Indian Government.

These schemes are available in public and private sector banks. You are required to have a savings account to opt for these schemes.

Both the above schemes, PMJJBY and PMSBY will not lapse if the premium amount is not paid.

PMJJBY and PMSBY schemes have tax saving benefits. This means the premium amount paid is free of taxes.

The premium sum charged towards the plan is deducted from the savings account associated each year on the auto-debit facility.

In case the balance in the bank associated is insufficient, then the policy will terminate. The insurer can reinstate the scheme once the payment of the outstanding premium sum is made.

*Note: It is suggested for all NRIs living in Canada that they know what is term insurance first and what its features are before they buy their ideal plan.

Even though both these schemes do not replace the need for a term insurance policy in our life, both these government-backed schemes help provide financial protection to the family in case of any eventuality. Moreover, the low-income group of individuals should consider investing in these schemes as it comes with a lower premium rate and ensure the right financial security for the family. One can apply for the schemes very easily by just filling the form.

Note: Check all the best term insurance plan in India.

Note: You should also check the benefits of term life insurance if you are planning to purchase the term insurance plan.

˜The insurers/plans mentioned are arranged in order of highest to lowest Sum Assured(SA) offered by Policybazaar’s insurer partners offering term insurance plans on our platform, as per ‘first year premium of life insurers as at 31.03.2025 report’ published by IRDAI.

Policybazaar does not endorse, rate or recommend any particular insurer or insurance product offered by any insurer. For complete list of insurers in India refer to the IRDAI website www.irdai.gov.in

Rs. 400/month is starting price for a 1 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age, rounded off to nearest 10.

Rs. 400/month (Rs.13/day) is starting price for a 1 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 230 is starting price for a 50 lakhs term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age, rounded off to nearest 10.

+Rs. 8/day is starting price for a 50 lakhs term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age, rounded off to nearest 10.

+Rs. 12/day is starting price for a 75 lakhs term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age, rounded off to nearest 10.

+Rs. 497/month is starting price for a 1.5 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 487/month is starting price for a 2 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 626/month is starting price for a 3 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 905/month is starting price for a 5 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. ₹361/month is the starting price for a ₹1 crore loan cover with an 8% interest rate for an 18-year-old male, non-smoker, with no pre-existing diseases, loan tenure up to 20 years, rounded off to the nearest 10

+Rs. 1,267/month is starting price for a 7 crore term life insurance for an 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

*The full refund of premium is available on availing the one-time option of refund of premium. Total premium paid for policy (paid for add-ons) will be the special exit value, payable on availing the one-time option of refund of premium if you wish to completely exit the policy.

+Rs. 447/month is starting price for a 1 crore term life insurance for an (NRI) 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs.679/month is starting price for a 2 crore term life insurance for an (NRI) 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 910/month is starting price for a 3 crore term life insurance for an (NRI) 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 1,374/month is starting price for a 5 crore term life insurance for an (NRI) 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

+Rs. 1,924month is starting price for a 7 crore term life insurance for an (NRI) 18 year-old male, non-smoker, with no pre-existing diseases, cover upto 30 years of age.

Women

+Rs. 400/month is Starting price for a 1 crore term life insurance for an 18 year-old Female, non-smoker, with no pre-existing diseases, cover upto 30 years of age, rounded off to nearest 10.

Rs. 461/month is the starting price for a 1 crore term life insurance for an 24 year-old female, non-smoker, with no pre-existing diseases, cover upto 54 years of age.

1,642/month is the starting price for a 1 crore term life insurance for an 44 year-old female, non-smoker, with no pre-existing diseases, cover upto 74 years of age.

Prices offered by the insurer are as per the approved insurance plans | #All savings and online discounts are provided by insurers as per IRDAI approved insurance plans | Standard Terms and Conditions Apply | **Tax Benefits are subject to changes in tax laws.| Policybazaar Insurance Brokers Private Limited

We will respond in the first instance within 30 minutes of the customers contacting us. 30-minute claim support service is for the purpose of giving reasonable assistance to the policyholder in pursuance of the claim. Settlement of claim (including cashless claim) is the responsibility of the insurer as per policy terms and conditions. The 30-minute claim support is subject to our operations not being impacted by a system failure or force majeure event or for reasons beyond our control. For further details, 24x7 Claims Support Helpline can be reached out at 1800-258-5881

For more details on risk factors, terms and conditions, please read the sales brochure carefully before concluding a sale

Policybazaar Insurance Brokers Private Limited | CIN: U74999HR2014PTC053454 | Registered Office - Plot No.119, Sector - 44, Gurgaon, Haryana – 122001 | Registration No. 742, Valid till 09/06/2027, License category- Composite Broker Visitors are hereby informed that their information submitted on the website may be shared with insurers. Product information is authentic and solely based on the information received from the insurers.

© Copyright 2008-2026 policybazaar.com. All Rights Reserved

˜ Policybazaar Promise reflects the guarantee offered by insurers. Price assurance is based on certifications shared by insurers with us.

Managing and reducing student loan debt involves proactive

Read more

Paying off student loans can feel like a long, exhausting

Read more

Tata AIA Shubh Rakshak Select is a special variant of Tata AIA

Read more

First-time homebuyers often make costly home loan insurance

Read more

To check your estimated social security benefits, create or log

Read moreInsurance

Calculators

Payment Methods

Secured With

Follow us on