Relationship manager

For every customer

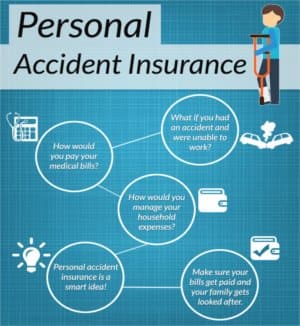

Personal Accident Insurance provides complete financial protection to the insured against uncertainties, such as accidental death, accidental bodily injuries, partial/total disabilities, and permanent/ temporary disabilities resulting from an accident. In the case of accidental death of the policyholder, the nominee gets 100% compensation from the insurer.

Select members you want to insure

A personal accident insurance policy covers physical loss to an individual due to accidental injuries leading to death or permanent/total disabilities. It is designed to pay compensation to the policyholder in case of an accident while travelling through rail, air, road, drowning, or due to a collision. Several health insurance plans also offer personal accident (PA) cover as an add-on.

A PA insurance policy not only pays compensation at the time of death but also financially secures the insured's family in the event of an accident. Moreover, it curtails financial constraints that may arise due to income loss resulting from accidental death or disabilities.

Accidents do not come knocking at the door. They can happen anytime, anywhere, and may result in minor to serious injuries. Any such uncertainty may lead to a financial crisis. While a minor accident can indispose an individual temporarily, major ones can have a severe impact on a person's life and their overall well-being. This is why buying a personal accident insurance policy is recommended.

A PA insurance policy will provide financial assistance to the policyholder against accidental death, bodily injuries and disabilities (partial/ total/ permanent/ temporary), irrespective of the intensity of the accident. Moreover, in case of the unfortunate accidental death of the policyholder, the insurer extends financial support to the insured's dependents by paying compensation to the legal heir of the policyholder.

Personal accident plans also offer various riders, such as accidental hospitalization cover, hospital confinement allowance, children's education cover, etc.

Here is a quick rundown of some of the major advantages of buying a personal accident insurance policy:

Check out the list of personal accident insurance plans in India:

| Personal Accident Insurance Plans | Entry Age (in years) | Coverage Amount Sum Insured (₹ in Rs) |

| Aditya Birla Activ Secure -Assure Personal Accident Plan | 5-65 years | Up to 12 times of annual gross income for an earning member 1 lakh to 20 crore |

| Bajaj Allianz Personal AccidentGuard Plan | 5-65 years | 10-25 lakh Up to 120 times of average monthly income |

| Care Secure Personal Accident Insurance Plan | 91 days-70 years | 15 lakh- to 25 crore |

| Cholamandalam Accident Protection Plan | 18-69 years | Family: 2.5-10 lakh Individual: 5 lakh to 13 crore |

| Digit Complete Care Policy | - | Up to 100% of the sum insured |

| Future Generali Personal Accident Suraksha Plan | 18-70 years | 50,000 to Up to 144 times of the annual income |

| HDFC ERGO Individual Personal Accident - Elite Plan | 18-70 years | 10,000 to up to 2.5-10 times of the annual incomecrore |

| ICICI Lombard Personal Protect Plan | 18-80 years | 3 to 25 lakh |

| IFFCO Tokio Individual Personal Accident Policy | 5-70 years | 100% of sum assured |

| Liberty Individual Personal Accident Policy | 18-70 years | 10 lakh to 1 crore |

| Magma HDI Individual Personal Accident Policy | 5-65 years | 1 lakh to - 60 times the monthly income or 5 crore, whichever is less |

| ManipalCigna Lifestyle Protection - Accident- Care Plan | 5-80 years | 50,000 to 10 crore |

| National Personal Accident Plan | 5-70 years | 72 months gross pay or Rs.10 lakh whichever is less. |

| New India Personal Accident Policy | 5-70 years | Up to 72 months of income |

| Niva Bupa Personal Accident Health Insurance Plan | 2-65 years | 5 lakh to 5 crore |

| Oriental Mediclaim Insurance Policy (Individual) | 18-65 years | 2 to 10 lakh |

| Raheja QBE Individual Personal Accident Insurance Policy | - | As per policy document |

| Reliance Personal Accident 360shield Plan | 30 days-80 years | 5 lakh to 25 crore |

| Royal Sundaram Individual Personal Accident Policy (Death & Disablement Only) | 5-65 years | 5 to 75 lakh |

| SBI Individual Personal Accident Insurance Plan | 18-65 years | 1-10 lakh to 1 crore |

| Star Accident Care Individual Insurance Policy | 18-70 years | 5-15 lakh onwards |

| Tata AIG Personal Accident Guard Plan | Upto 65 years | 5 lakh to 1 crore |

| United India Individual Personal Accident Plan | 5-70 years | 25,000 to 10 lakh |

| Universal Sompo Individual Personal Accident Policy | 5-65 years | 10 times of the annual income |

| Zuno (Formerly Edelweiss) HealthPlus Policy | 91 days onwards with no upper limit | 5,000 to 5 crore |

| Zurich Kotak Accident Care Plan | 5-65 years onwards | Up to 10 times of the annual income |

*Disclaimer: The list mentioned is according to the alphabetical order of the insurance companies. Policybazaar does not endorse, rate or recommend any particular insurer or insurance product offered by any insurer. This list of plans listed here comprise of insurance products offered by all the insurance partners of Policybazaar. For complete list of insurers in India, refer to the Insurance Regulatory and Development Authority of India website www.irdai.gov.in.

You May Also Like to Read: Kinds of Health Insurance

A personal accident insurance policy covers the following:

In case an accident leads to the death of the policyholder, the entire sum assured is paid to the nominee or the legal heir.

In case an accident results in permanent disabilities or lifelong total impairment, such as loss of both limbs, then a specified sum insured amount is paid to the policyholder.

If an accident results in permanent partial disabilities, then a certain percentage (up to 100%) of the benefit is paid to the policyholder.

In case the insured meets with an accident leading to temporary total disabilities and is bedridden, then the insurer will pay a weekly allowance to compensate the loss of income. The insured can utilize this claim amount to pay the EMIs.

If the policyholder ends up losing the job due to accidental injuries, then the insurer will compensate a fixed amount for the loss of income.

In case of an unexpected demise of the policyholder due to an accident, the cost of education of the dependent child is covered up to a specified limit.

In the event of unexpected demise or lifelong disabilities of the policyholder due to an accident, a lump sum amount is paid to repay the loan amount.

In case of accidental death of the policyholder, the nominee would receive compensation for the expenses incurred on repatriation and transportation of the mortal remains from the site of the accident to the hospital, home or the cremation ground.

The insurer also pays for the expenses incurred on the religious ceremonies related to the cremation of the policyholder in case of accidental death.

In case of fractured bones or any bone damage due to an accident, a fixed compensation is paid under the policy.

The insurer pays compensation to the policyholder for burns resulting from an accident.

If the policyholder is hospitalized due to an accident, the insurance company will pay for the medical expenses incurred during the hospital stay.

It covers the medical expenses incurred on availing life support by the policyholder during accidental hospitalization.

It pays for ambulance charges used to carry the insured post-accident to the hospital.

It covers the actual transportation expenditure incurred by the immediate family member to reach the hospital where the insured is admitted after the accident. This cover is applicable only if the insured is hospitalized in another city.

A daily cash allowance is paid to the insured in case of an accidental hospitalization. However, the coverage is limited to a certain number of days as specified in the policy terms and conditions.

In case of permanent total disabilities or dismemberment due to an accident, the insurer pays for the expenses incurred on modifying the house and/or vehicle of the insured.

Personal accident policies do not cover death or disabilities due to:

As a thumb rule, a person should opt for a personal accident cover of at least 100 times of your monthly income. For example, if Mohan's current earnings are ₹10,000, then he should buy a personal accident cover of ₹10,00,000. Doing so will ensure that all the eventualities resulting from an accident, such as child education expenses, loan repayment, marriage expenses, regular earnings for the spouse, etc., are taken care of by the insurance policy.

The premium of a personal accident policy is decided on the basis of the applicant's occupation. Generally, occupational risks under personal accident insurance can be segmented into the following three categories:

| Class 1= Low-Risk | Class 2= High-Risk | Class 3= Very High Risk |

| Accountants Lawyers Bankers Doctors Teachers Architects Administrative/ managing functions |

Money carrying employees Builders Contractors Machine operators Garage mechanic Manual labour Veterinary doctors Contractors |

Journalists People working in explosive industries Mountaineers Mine workers Jockey Professional river rafters Big game hunters Circus performers |

A personal accident insurance policy covers loss of life or disabilities due to accidents. But a life insurance policy covers the death of a policyholder irrespective of the cause of death. The major differences between accidental insurance and life insurance policies are listed below:

| Coverage | Accidental Death Insurance | Life Insurance |

| Death from illness or disease | No | Yes |

| Accidental death | Yes | Yes |

| Permanent total disabilities | Yes | No |

| Partial disabilities | Yes | No |

A critical illness insurance policy pays a lump sum amount to the policyholder to carry out the medical treatment of a listed critical illness. There is a survival period clause to avail the benefits. But a personal accidental insurance policy covers partial or total disabilities and accidental death of the insured. Check out the key differences between PA insurance and critical illness cover:

| Parameters | Personal Accident Insurance | Critical Illness Insurance |

| Importance | Compensation is only provided for accidental death and disabilities | It pays a lump sum amount on the diagnosis of critical illnesses like kidney failure, cancer, paralysis, etc. |

| Coverage | It does not cover diseases or illnesses. | It covers specified critical illnesses like cancer, tuberculosis, etc. |

| Waiting Period | No waiting period | Up to 3 months of waiting period |

| Medical Check-up | No Required | Required |

A term insurance policy covers the death of the policyholder due to natural reasons or accidental causes. But a personal accident insurance policy would only offer coverage for death and disabilities caused by an accident. It would not cover claims arising due to natural deaths.

To initiate the claim process for personal accident insurance, inform the insurance provider within the specified time frame. The insurer may provide a claim reference number. The following information is required to be submitted to the insurer while intimating a claim:

It is essential that these details are also known to the family members or dependents of the policyholder(including spouse), as an unexpected event such as the demise of the insured may leave them unaware of what to do next.

Submit all the required documents to the insurer. The insurer will verify the documents and pay the claim amount to the policyholder or the nominee as the case may be.

Medical emergencies arrive unannounced and can leave you with

Read more

Health insurance is an essential part of financial planning today

Read more

Life after retirement should be about relaxation and not worrying

Read more

As people age, their health deteriorates, making them more

Read more

For years, health insurance has been synonymous with hefty medical

Read more*We will respond in the first instance within 30 minutes of the customers contacting us. 30-minute claim support service is for the purpose of giving reasonable assistance to the policyholder in pursuance of the claim. Settlement of claim (including cashless claim) is the responsibility of the insurer as per policy terms and conditions. The 30- minute claim support is subject to our operations not being impacted by a system failure or force majeure event or for reasons beyond our control. For further details, 24x7 Claims Support Helpline can be reached out at 1800-258-5881.

*Product information is authentic and solely based on the information received from the Insurer. Policybazaar is acting only as a facilitator and claims settlement shall be at the sole discretion of the Insurer. Policybazaar does not provide any medical or surgical advice or diagnosis and is not responsible for your interactions / treatment by a medical practitioner/hospital. Please consult a registered medical practitioner for any medical or surgical advice. The Information that you obtain or receive from Policybazaar, and its employees, or otherwise on the Website is for informational purposes only. As per the Insurance guidelines, you are allowed to cancel the policy with-in 30 days from the date of Issuance of policy.This option is available incase of policies with a term of one year or more.

*All the health insurance plans cover hospitalization expenses including COVID-19 treatment cover up to the specified limits. You can also buy specific COVID-19 health insurance policies such as Corona Kavach Policy and Corona Rakshak policy.

**All savings and online discounts are provided by insurers as per IRDAI approved insurance plans. #Tax Benefits are subject to changes in tax laws. GST Exemptions depend on fulfilment of qualification criteria and submission of relevant documents.

*₹1748/month is the starting price for a 1 crore health insurance for an 18-year-old male, with no pre-existing diseases. Discount on renewal premium is subject to the number of wellness points earned in the health insurance policy. For more details about the plans, please read the sale brochure carefully to get upto 100% discount on renewal premium.

*₹400/month is the starting price for ₹ 5 lakh Health insurance for a 30 year old male & 29 years old female, living in Delhi with no pre-existing diseases

*₹541/month is the starting price for ₹ 10 lakh Health insurance for a 30 year old male & 29 years old female, living in Delhi with no pre-existing diseases

*₹762/month is the starting price for ₹ 1 Crore Health insurance for a 30 year old male & 29 years old female, living in Delhi with no pre-existing diseases

*₹243/month(₹ 8/day) is the starting price for a 5 lakh health insurance for a 20-year-old male, non-smoker, living in Bengaluru with no pre-existing diseases

*₹2020/month is the starting price for ₹ 1 Cr Health insurance for a 50 year old male & 50 years old female, living in Bangalore with no pre-existing diseases rounded off to nearest 10.

*₹390/month (₹13 per day) is starting price for 1 cr. Health insurance for 25 years old male, with pre-existing diseases, residing from tier 1 city rounded off to the nearest 10.

*No medical tests are required unless requested by the insurer’s underwriter. In-case of pre-existing diseases relevant medical proof would be required as per the terms and condition of the policy opted.

*The values taken for effective cost calculation are indicative values and may change as per the selected plan.

*Coverage upto double the amount of Sum Insured is available on certain covers for a minimum plan of Rs. 5 Lakh on the first claim only to an individual of upto 45 years of age with no pre-existing diseases. The benefit is available with or without extra cost depending on the plan chosen.

*Coverage of pre-existing diseases is provided by insurer as per their underwriting policy.

*The scope of coverage may vary from plan to plan.

~Source: Google Review Rating available on:- http://bit.ly/3J20bXZ

##On ground claim assistance is available in 114 cities

Tax Benefits are subject to changes in tax laws. GST Exemption depends on fulfilment of qualification criteria and submission of relevant documents as required by the insurers. For more details on risk factors, terms and conditions, please read the sales brochure and applicable rules and regulation carefully before concluding a sale.

STANDARD TERMS AND CONDITIONS APPLY. For more details on risk factors, terms and conditions, please read the sales brochure carefully before concluding a sale.

Policybazaar is a registered Composite Broker |Registration No. 742, Valid till 09/06/2027, License category- Composite Broker| Visitors are hereby informed that their information submitted on the website may be shared with insurers.

Policybazaar Insurance Brokers Private Limited | CIN: U74999HR2014PTC053454 | Registered Office - Plot No.119, Sector - 44, Gurgaon, Haryana - 122001 Contact Us | Legal and Admin Policies

© Copyright 2008-2025 policybazaar.com. All Rights Reserved.

Insurance

Calculators

Payment Methods

Secured With

Follow us on